FHA vs. USDA in Louisiana: Which Loan is Right for You?

If you're a first-time homebuyer in Louisiana, you've probably heard a lot about FHA loans. They're the go-to government-backed option for many buyers, especially those with credit scores that need a little TLC. But here's the thing. FHA isn't your only path to homeownership, and for thousands of Louisiana families, there's an even better option hiding in plain sight: the USDA loan.

Yep, you read that right. USDA loans aren't just for farmers in the middle of nowhere. In Louisiana, many suburban and rural areas qualify for this incredible 0% down payment program. So which loan is actually right for you? Let's break it down in plain English.

What is an FHA Loan?

FHA loans are insured by the Federal Housing Administration and have been helping Americans buy homes since the 1930s. Here's what you need to know:

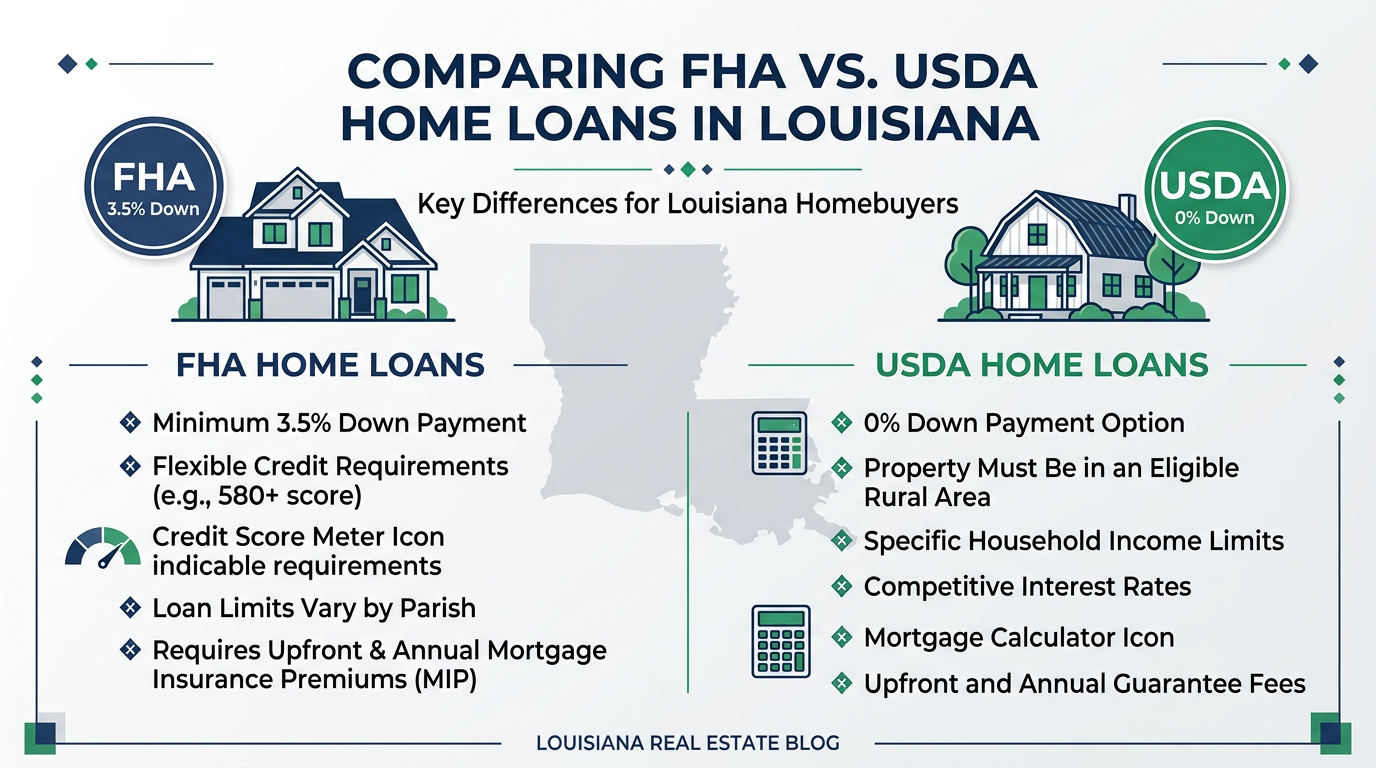

- Credit Requirements: You can qualify with a credit score as low as 580 to put down 3.5%, or even 500 with a 10% down payment. That flexibility is a game-changer if your credit has taken some hits.

- Down Payment: The minimum is 3.5% of the purchase price. On a $250,000 home, that's $8,750.

- Mortgage Insurance: You'll pay two types. An upfront premium (1.75% of the loan) rolled into your mortgage, plus monthly premiums. This insurance stays for the life of the loan in most cases.

- Property Types: FHA works for single-family homes, condos, and even some multi-family properties (up to 4 units) if you plan to live in one unit.

What is a USDA Loan?

USDA Rural Development loans are designed to boost homeownership in eligible rural and suburban areas, and Louisiana has plenty of them. Here's the scoop:

- Credit Requirements: While USDA technically doesn't set a minimum, most lenders want to see a 640 credit score or higher.

- Down Payment: Zero. Nada. Zilch. You can finance 100% of the home's purchase price.

- Mortgage Insurance: There's an upfront guarantee fee (1% of the loan) and an annual fee (0.35%), but these are typically lower than FHA costs.

- Income Limits: Your household income can't exceed 115% of the area median income. In most Louisiana parishes, that's around $103,500 for a family of 1-4 people.

- Location: The property must be in an eligible rural or suburban area. Spoiler alert: Many areas you wouldn't think of as "rural" actually qualify including parts of parishes surrounding Baton Rouge, Lafayette, Lake Charles, and Shreveport.

FHA vs. USDA: Quick Comparison

| Feature | FHA Loan | USDA Loan |

|---|---|---|

| Minimum Down Payment | 3.5% | 0% |

| Credit Score Minimum | 580 (or 500 with 10% down) | 640 (typically) |

| Mortgage Insurance | Higher, lifelong | Lower, can be removed |

| Geographic Limits | None | Eligible rural/suburban areas only |

| Income Limits | None | 115% of area median income |

| Property Types | More flexible | Single-family, primary residence only |

Which Loan is Right for You?

Here's my straightforward take: If you're buying in an eligible USDA area and your income qualifies, USDA is usually the winner. You keep more cash in your pocket at closing (hello, zero down!), and your monthly mortgage insurance costs are typically lower.

Choose FHA if:

- You're buying in a major city center (like downtown New Orleans) that doesn't qualify for USDA

- Your income exceeds USDA limits

- You want to buy a duplex or triplex

- Your credit score is below 640

Choose USDA if:

- The property is in an eligible area (check the USDA eligibility map)

- Your household income fits within the limits

- You want to preserve your savings for moving expenses or home improvements

- You have decent credit (640+)

Ready to Find Your Perfect Loan?

Here's the truth, every buyer's situation is unique. Maybe you're self-employed, or you're trying to decide between a fixer-upper in the city or a move-in-ready home in the suburbs. That's where having a local mortgage expert in your corner makes all the difference.

I've helped hundreds of Louisiana families navigate both FHA and USDA loans, and I know exactly which neighborhoods qualify and how to structure your application for the best shot at approval.

Let's figure out your best path forward together. Whether FHA, USDA, VA, or conventional is your golden ticket, I'll find the loan that saves you the most money and gets you into your dream home faster.